Investors often weigh exposure between Nifty 50 and Bank Nifty, especially in volatile markets. In February, while Nifty fell nearly 6% from its highs, Bank Nifty dipped only 3.3%, strongly defending the 48,000 level—highlighting the impact of smart sectoral allocation. Let us see what history indicates to assess where the index might be headed.

Bank Nifty’s Consistent Outperformance

A closer look at the past 19 years shows that Bank Nifty outperformed Nifty 50 in 12 of those years (63.16% of the time). Some of the best performing years—such as 2009, 2014, and 2021—saw significant alpha generation by Bank Nifty, proving its ability to deliver strong upside moves.

Is the Recent Underperformance a Buying Opportunity?

In 2024, Bank Nifty has underperformed Nifty 50 by -9.87%, raising the possibility that it might be due for a rebound. History shows that such periods of lagging performance have often been followed by strong recoveries, making this an area worth monitoring. Some of the factors supporting the same are shown below:

1. Valuations Suggest Room for Growth

Currently, Bank Nifty’s P/E ratio stands at 13.6x, well below its historical average of 22x, whereas Nifty 50’s P/E is at 21x, in line with its 20-year long-term average. This significant undervaluation might indicate a potential rotation into Bank Nifty.

When trading below its historical P/E, Bank Nifty has delivered 15.51% 3-year returns, with an alpha of 4.90% over Nifty 50

2.Earnings Growth Supports Long-Term Strength

- 7Yrs EPS CAGR of Bank Nifty is 24.5% against price growth of 11.3%.

- 10 Yr EPS CAGR is 14.8% against price growth of just 10.9%.

Both numbers suggest that prices have lagged earnings and could play catch-up in the coming years.

With EPS growth continuing at a better than average healthy pace as seen above, Bank Nifty appears to be in a stronger earnings cycle than before, which may support future price appreciation.

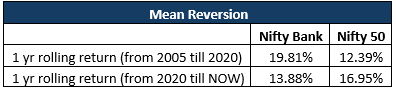

3.Mean reversion could drive a rebound

While the average 1Y rolling return pre-COVID was ~20% for Bank Nifty, it is just ~14% post-COVID suggesting that there may be scope for reverting to the mean. This can also indicate that Bank Nifty may have to give more than average returns to compensate for the same.

Conclusion

Given its current undervaluation and strong earnings growth, investors seeking long-term opportunities may find merit in increasing exposure to this index, particularly when historical cycles suggest potential upside now while market volatility persists.

Subscribe on LinkedIn